Real Estate News

If you ask anyone involved in real estate how the market is, you are likely to hear

something regarding mortgage rates and how they have recently risen, instead of falling. This is certainly part of the reason the 2026 real estate market has been sluggish. At the time of writing, mortgage rates are averaging around 6.5%. Compared to the time of COVID (March 2020) and the time shortly after, this is a high rate. With a little perspective, we can see that 6.5% is much closer to average, even a little lower, historically.

something regarding mortgage rates and how they have recently risen, instead of falling. This is certainly part of the reason the 2026 real estate market has been sluggish. At the time of writing, mortgage rates are averaging around 6.5%. Compared to the time of COVID (March 2020) and the time shortly after, this is a high rate. With a little perspective, we can see that 6.5% is much closer to average, even a little lower, historically.

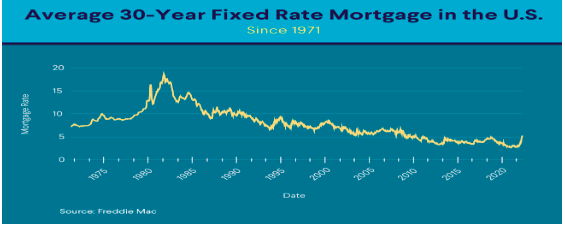

Check out this chart from So-Fi below. You can see where mortgage rates

peaked near 20% in the early 1980’s. Several local Realtors have told me how difficult it was to both purchase and sell real estate during this era. Many agents sold land and timber just to get by. The residential market was very slow and trying during this time.

peaked near 20% in the early 1980’s. Several local Realtors have told me how difficult it was to both purchase and sell real estate during this era. Many agents sold land and timber just to get by. The residential market was very slow and trying during this time.

A significant difference between now and then is that median home price in June

of 1982 was only $69,300. (census.gov). The median home price today is $423,740 (nar.realtor). Let’s look at the difference in payments now and then: A mortgage payment today, with very good credit, five percent down, at $423,740, 6.5% interest, in Newnan, would estimate to be $2,890 a month (including taxes and insurance).

of 1982 was only $69,300. (census.gov). The median home price today is $423,740 (nar.realtor). Let’s look at the difference in payments now and then: A mortgage payment today, with very good credit, five percent down, at $423,740, 6.5% interest, in Newnan, would estimate to be $2,890 a month (including taxes and insurance).

A mortgage payment in June of 1982, with very good credit, five percent down, at $69,300, 16.5% interest, in Newnan, would estimate to be around $1,258 a month (including taxes and insurance). This is nearly half of what a payment today would be at 1/6 of the sales price. The mortgage, or interest rate, is a very powerful factor in the real estate market. The bigger issue today is how the cost of everything, along with prices, has increased dramatically since 1982.

If you are waiting for rates to drop back to the two and three percent range again

to purchase, you will likely never see that. With a little perspective, you may discover that it may not be a bad time to purchase after all. I would suggest centering your decision to purchase, if possible, on other factors like where you are in your life, job, family, lifestyle, etc. rather than based on mortgage rates and predictions.

to purchase, you will likely never see that. With a little perspective, you may discover that it may not be a bad time to purchase after all. I would suggest centering your decision to purchase, if possible, on other factors like where you are in your life, job, family, lifestyle, etc. rather than based on mortgage rates and predictions.